Welcome to our November 24 Property Market Snapshot

November at a glance

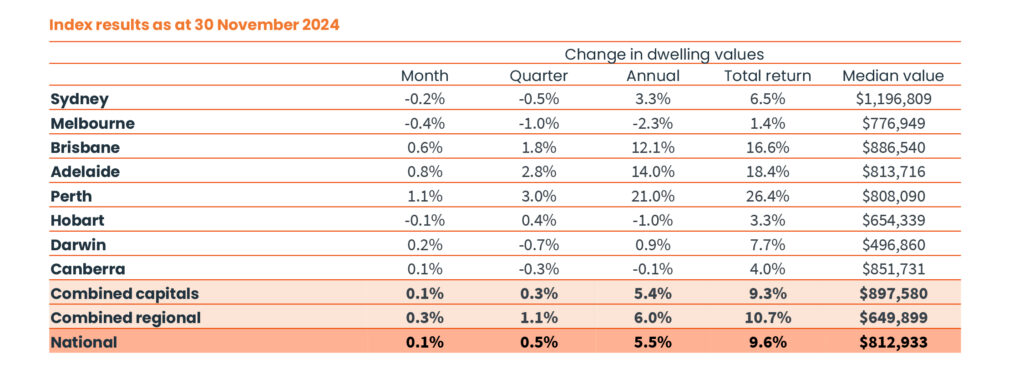

- In November, Home Values saw a 0.1% rise, marking the 22nd month of growth since February last year.

- Mid-sized capitals reflected the slight positive movement, led by Perth showing a 1.1% rise over the month.

- This was offset by declines in Melbourne (-0.4%), Sydney (-0.2%), and regional Victoria (-0.1%).

- Annual growth in national home values continued to ease, reducing to 5.5% over the 12 months ending November.

Dwelling values

Dwelling values in November 2024 saw continued softening in Sydney, with home values declining by -0.2%. This marked the second consecutive month of decline after a -0.2% drop in October. The downturn has been led by the upper quartile of the market, reflecting weaker conditions in the more expensive areas.

In contrast, affordable segments showed resilience, with the combined regional index rising by 1.1% over the quarter compared to a modest 0.3% lift across the combined capitals. Despite this, the mid-sized capitals such as Brisbane and Adelaide, which previously led growth, also lost momentum, with quarterly growth slowing to 1.8% and 2.8%, respectively.

Stock levels increased, with capital city listings up by 16% since the end of winter, including a notable 33% rise in Perth. However, purchasing activity waned, with capital city home sales over the past three months declining by -4.6% compared to a year ago and -2.0% below the five-year average. In Sydney, sales activity was particularly weak, down -15.4% compared to the previous year.

Selling conditions deteriorated further with higher inventory levels and lower buyer demand. Auction clearance rates in combined capitals remained below 60% since mid-October, and median days on market for private treaty sales increased, indicating a slower market.

Rental market

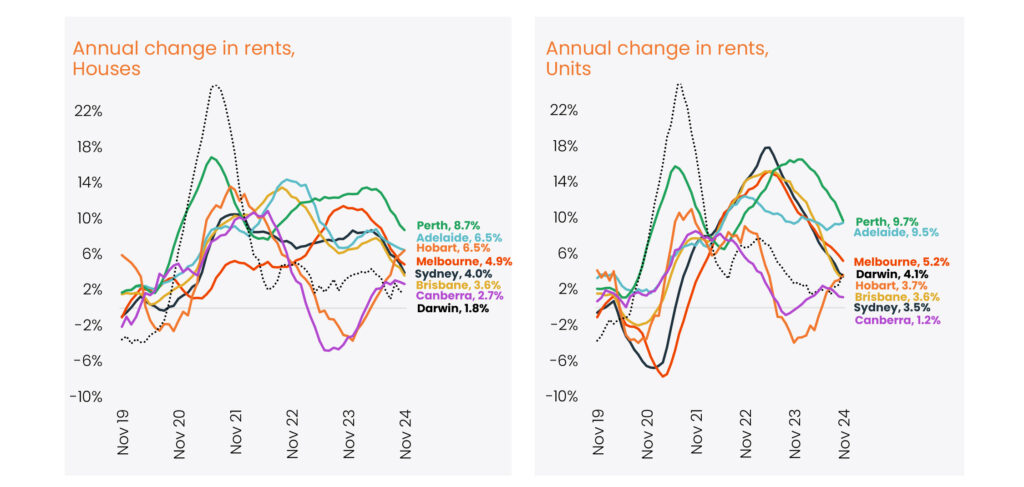

National rents increased modestly by 0.2% in November, maintaining a relatively flat growth trend. This represents an annual rental growth rate of 5.3%, the smallest increase since April 2021. The rental market continues to soften, marking a significant slowdown compared to the rapid rises seen in previous years.

The unit sector has been particularly weak, with rents falling over the past three months in key markets, including Sydney (-0.6%), Melbourne (-0.4%), and Brisbane (-0.3%). In November, rents in Perth’s unit sector remained the strongest among capitals, recording an annual growth of 9.7%, though this too reflects a deceleration from the peak of 16.6% earlier in 2024.

As rental growth eases, gross rental yields are facing downward pressure. The gross yield for all capital city dwellings held at 3.0% in November, considerably lower than the pre-pandemic decade average of 3.9%. This reflects the impact of both flattening rents and high property prices on investor returns.

Outlook

Between rising advertised stock levels, slowing purchasing activity and the loss of momentum in value The housing market outlook for late 2024 remains subdued due to rising stock levels, slowing purchasing activity, and a continued loss of momentum in value growth, indicating a weaker market environment than earlier in the year.

There is, however, a trend towards lower inflation. This could mean a cut in interest rates in the first quarter of 2025. On the brighter side, there are signs of easing inflation, which could pave the way for a potential interest rate cut in the first quarter of 2025. Labour markets remain robust, with the national unemployment rate steady at 4.1% over the past two months, supported by strong job growth and record-high workforce participation.

Dwelling commencements are slowing, with approvals falling below average and the number of homes under construction in decline. While affordability challenges continue to impact much of the Australian housing market, these supply-side constraints are likely to underpin housing prices, offering some resilience against further downward pressure.

CLICK HERE TO DOWNLOAD THE FULL REPORT

Disclaimer: The opinions posted within this blog are those of the writer and do not necessarily reflect the views of Better Homes and Gardens® Real Estate, others employed by Better Homes and Gardens® Real Estate or the organisations with which the network is affiliated. The author takes full responsibility for his opinions and does not hold Better Homes and Gardens® Real Estate or any third party responsible for anything in the posted content. The author freely admits that his views may not be the same as those of his colleagues, or third parties associated with the Better Homes and Gardens® Real Estate network.